Question: How much did mortgage rates drop after the Fed cut rates last week?

Answer:

The Fed Cut Rates and Mortgage Rates…Went Up

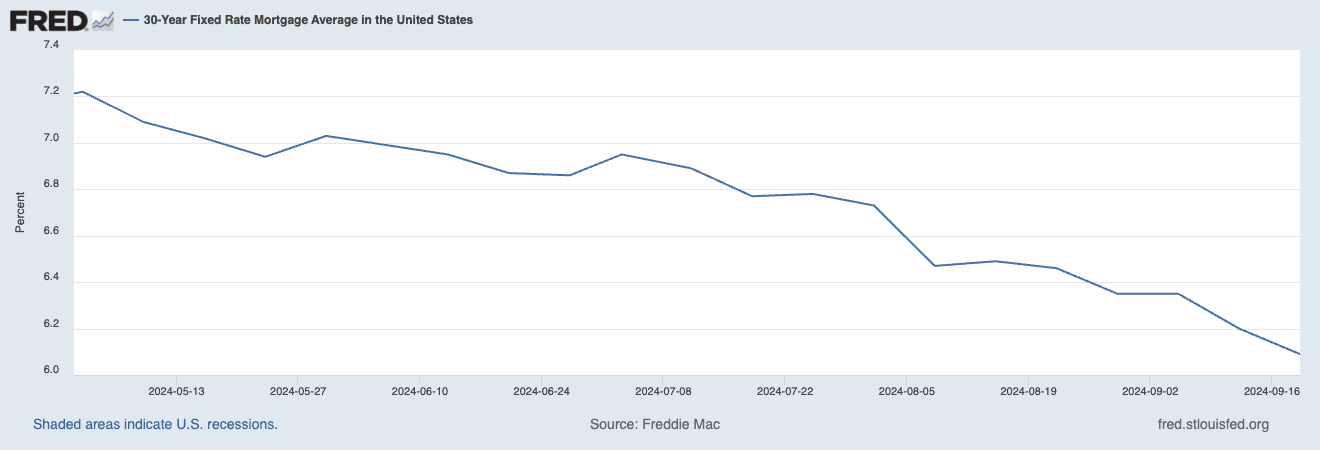

Last week, the Federal Reserve cut the fed funds rate by 0.5%, more than the 0.25% some expected. Great news for mortgage rates, right? Wrong.

Despite the large rate cut by the Fed, mortgage rates actually increased each of the next two days. Why?

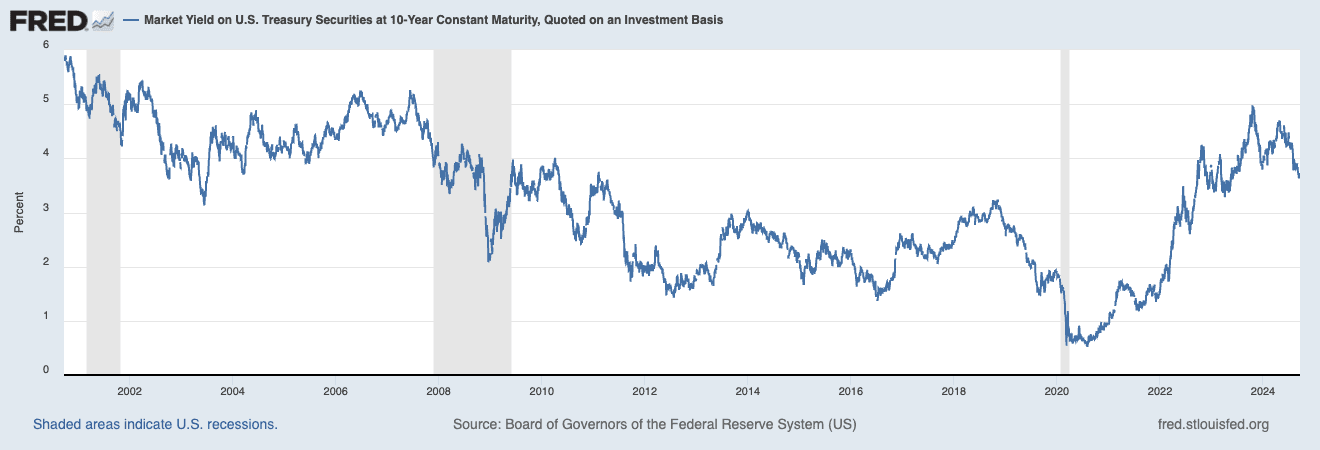

To understand this, you need to understand that mortgage rates are not directly tied to the fed funds rate but are influenced by something else: the 10-year Treasury yield.

The Fed Funds Rate vs. Mortgage Rates

The fed funds rate is the interest rate banks charge each other for overnight loans. The Federal Reserve adjusts this rate to control inflation and guide economic growth. When they cut the rate, it makes borrowing cheaper in the short term, encouraging spending and investment.

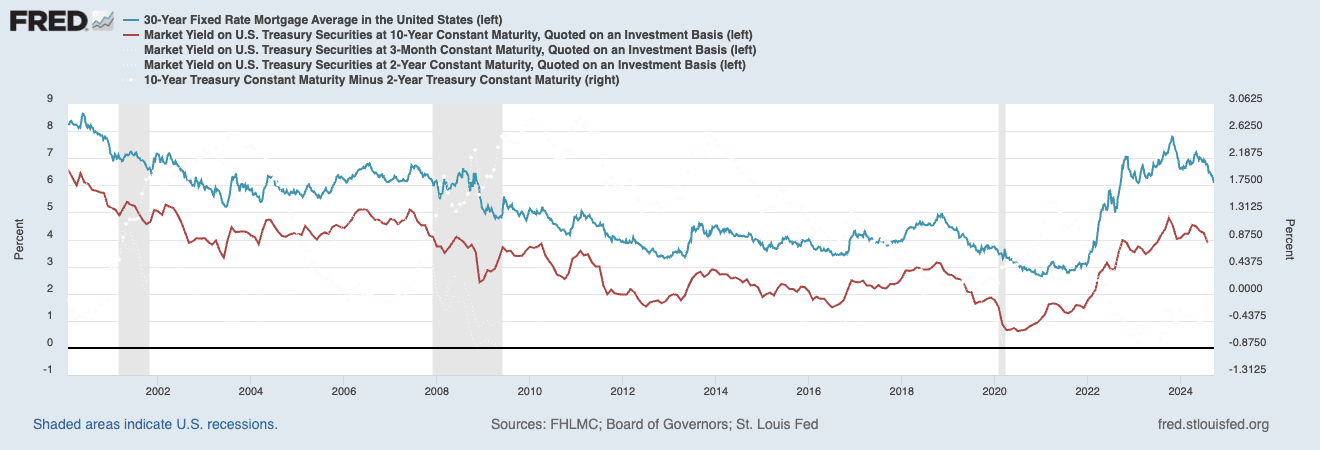

However, long-term interest rates, like mortgage rates, don’t directly follow the fed funds rate. Instead, they are more closely linked to the yield on the 10-year Treasury note. The 10-year Treasury is market driven, as opposed to the fed fund rate controlled by the Federal Reserve, and its yield reflects investor expectations about future inflation, economic growth, and overall risk in the economy.

Note: While mortgage rates aren’t directly tied to the fed funds rate, other consumer rates like credit cards, auto loans, and the interest rates on savings accounts are.

Mortgage Rates Didn’t Fall because the 10-year Treasury Yield Rose

Even as the Fed cut rates, the 10-year Treasury yield increased, moving from 3.65% to 3.71%. Mortgage rates followed suit. It can be hard to say exactly why financial markets behave in certain ways, but it’s quite possible that investors were looking for more definitive signs from Jerome Powell (Fed Chair) in his speech to indicate that more rate cuts were coming. It may also indicate ongoing concerns by investors over the longer-term health of the economy and the stabilization of inflation.

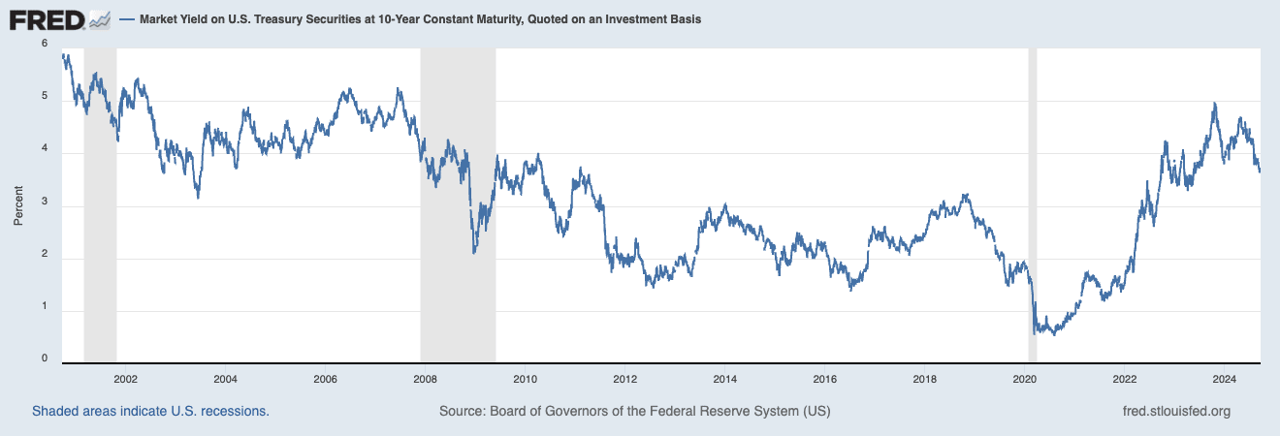

Rates Were Already Down to 18-Month Lows

I mentioned earlier that the 10-tear Treasury yield, which drives mortgage rates, is market-driven (like stock prices) so the expectation for last week’s Fed rate cut had already been priced into the market once it became evident the Fed was going to cut rates at last week’s meeting. In fact, over the last 4-8 weeks, mortgage rates have fallen steadily by about 1.5% and are lower than they’ve been in 18+ months.

What to Expect? What is a “Normal” Mortgage Rate?

Since 2008, we’ve gotten used to unusually low interest rates, in historical terms. The 10-year Treasury yield fell to as low as 0.52% in 2020, during the peak of pandemic uncertainty. Today, the yield is around 3.7%, which seems high by recent standards but is relatively normal if we look at pre-2008 levels, when yields were often in the 4-6% range.

This suggests that even though the Fed has started cutting rates, we may not see mortgage rates drop much further. If we are returning to a more “normal” economic environment, where rates resemble pre-2008 levels, then current mortgage rates may already be close to as low as they will go.

Keep an Eye on the Mortgage Rate and 10-year Treasury Spread

The spread between the 10-year Treasury yield and mortgage rates is currently much higher than the historical average. Typically, the spread is about 1.5-2%, but recently it’s been 2.5-3%+. This wider gap is primarily due to reduced demand for mortgage-backed securities (MBS). In the past, the Federal Reserve played a significant role in buying MBS as part of its quantitative easing program, which helped keep mortgage rates lower by increasing demand for mortgage securities. However, since 2022, the Fed has scaled back its MBS purchases, leading to a decline in demand and thus pushing up prices (mortgage rates).

Additionally, other large investors, including foreign countries and funds, have shown less interest in MBS, further reducing demand. This shift has pushed investors to require higher returns (or yields) for holding MBS, which has driven up mortgage rates.

This means that even though Treasury yields might fall, mortgage rates may not follow suit as closely as they have in the past.

Thank you and Refinance Opportunity

Thank you to Jake Ryon of First Home Mortgage for his support in drafting this column and making sense of complex market dynamics. If you have questions about what’s happening in the mortgage market or would like a recommendation to an excellent local loan officer, I recommend reaching out to Jake.

If you purchased a home recently with a rate near or above 7%, you may be in a great position to refinance and bring your monthly mortgage payments down, without bringing any additional money to the table. Send Jake an email at [email protected] and he can run numbers for you to see if it makes sense.

If you’d like to discuss buying, selling, investing, or renting, don’t hesitate to reach out to me at [email protected].