Question: Will housing inventory come back to the market after this spring’s big drop?

Answer: If you’re tired of seeing me write about the low housing supply, I don’t blame you, but it’s the most important factor in our housing market and will likely continue to be for the foreseeable future. This week’s analysis digs into just how big the gap in expected vs actual housing inventory was this spring (Coronavirus) and what the future might look like as that inventory (hopefully) rolls back into the market.

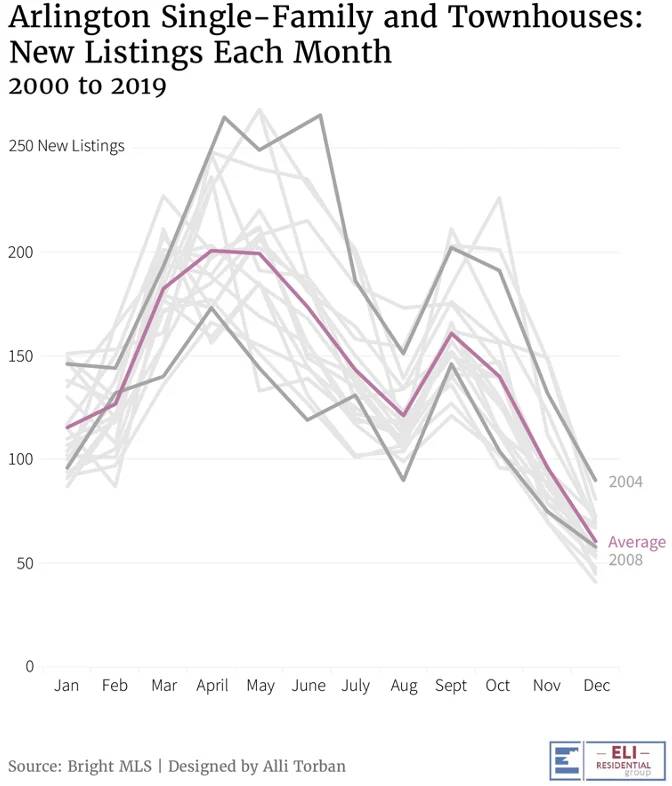

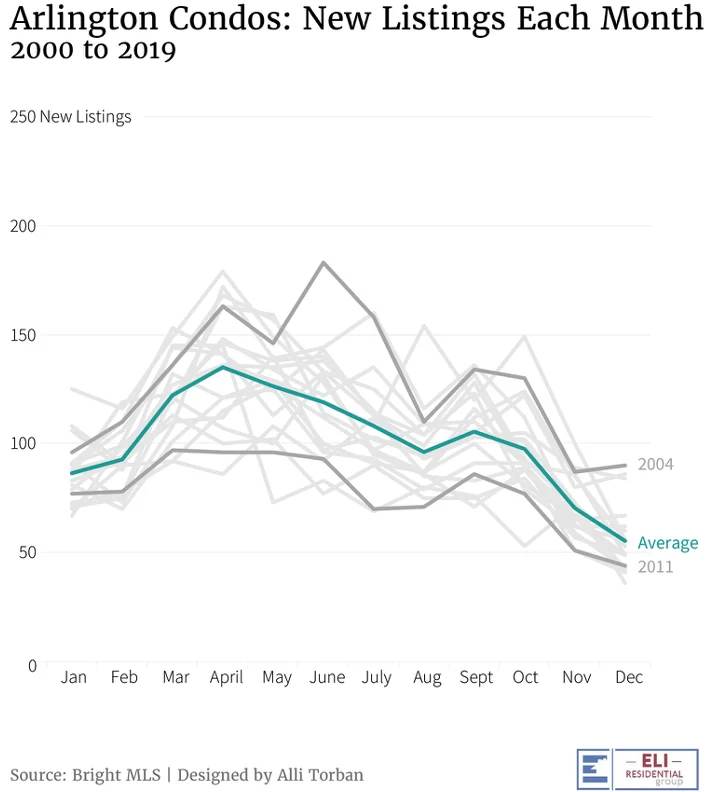

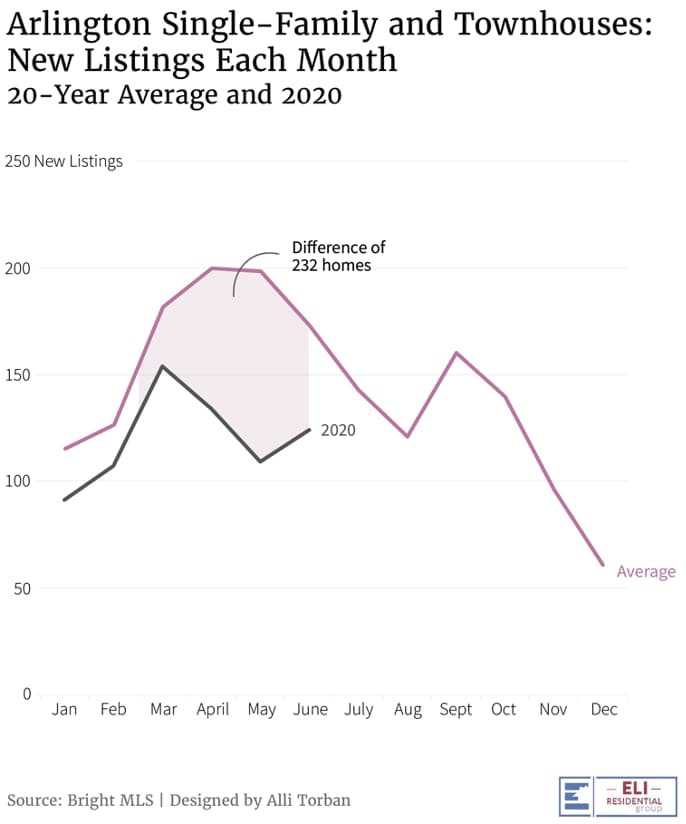

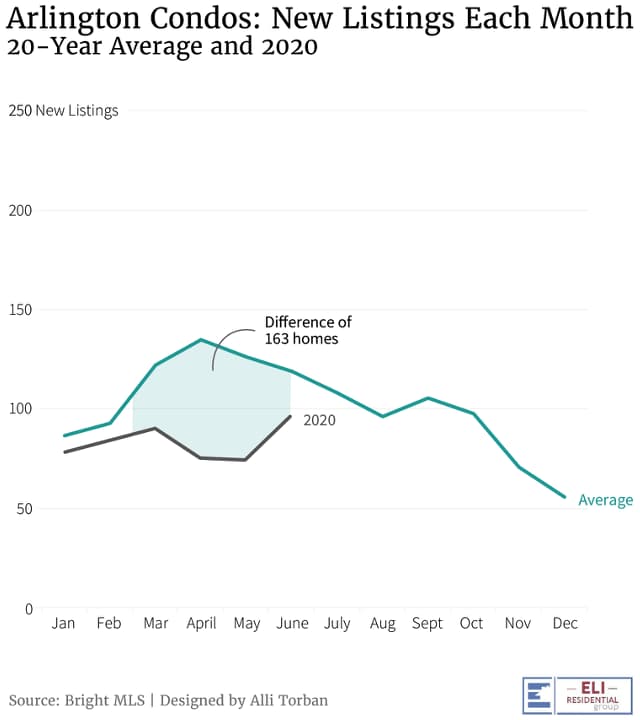

20 Years of (mostly) Consistent Housing Inventory

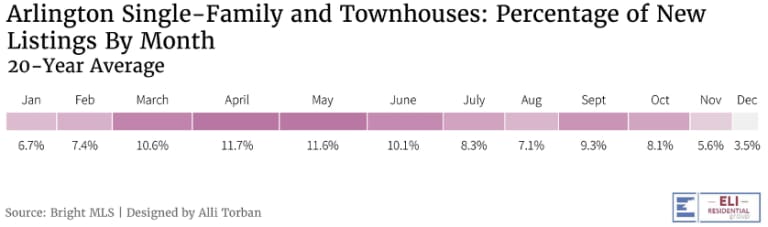

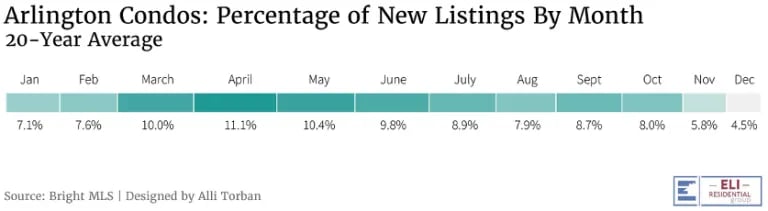

The pace and distribution of new inventory in Arlington has been pretty consistent over the last 20 years. Inventory peaks in the spring, with about 1/3 of new listings hitting the market from March-May and then steadily declines to annual lows during the holidays, with a slight “fall bump.”

Where It All Went Wrong

Like everything else in 2020, housing inventory suffered tremendously during the COVID-19 outbreak and associated lockdowns. In the months prior to COVID-19 (December-February) the number of new listings seemed to be on track to return to, or close to, our 20-year average after a down year in 2019 (due to the Amazon HQ2 announcement). However, from March-June 2020 we ended up down 232 single-family/townhouse listings and 163 condo listings compared to the 20-year average.

My Hypothesis: Hope is on the Horizon

As shown in the first charts, there is a downward trajectory in new listings after new inventory peaks in April and May. We’re seeing drastically different market behavior this year, with a sharp positive trajectory in new listings in June (continuing in July, but not charted due to incomplete data at time of publishing).

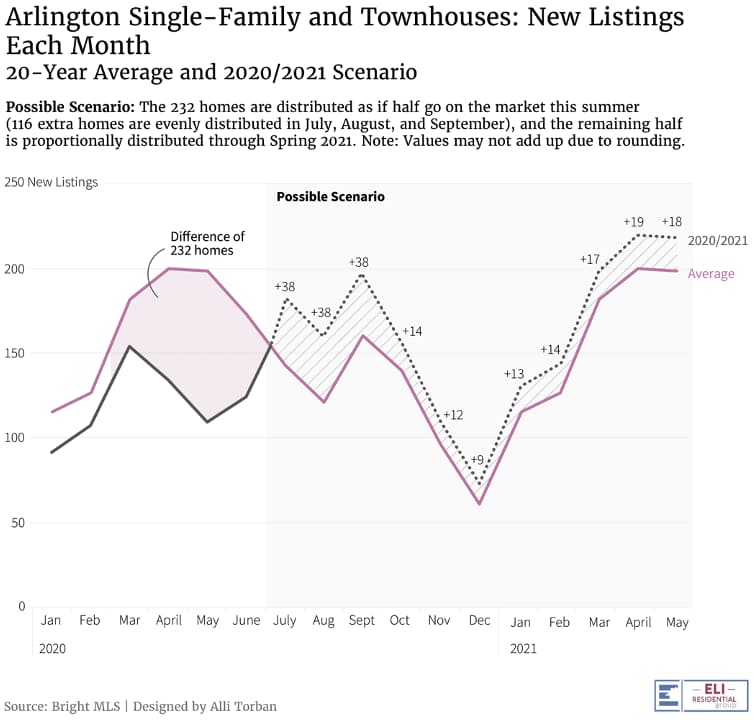

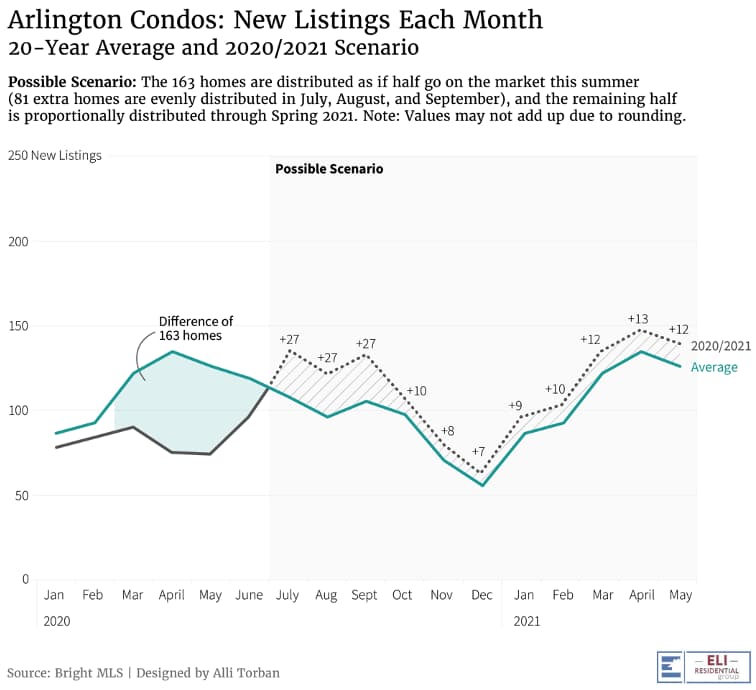

My hypothesis is that the majority of homeowners who planned to sell this spring and held off due to Coronavirus still have every intention of selling and will likely do so between this summer and spring 2021, resulting in an above-average rate of new listings per month over the next 9 months, barring any major shifts in Coronavirus related market behavior.

I also think that more of the pent-up inventory will be released this summer/early fall because of how strong the market currently is (low interest rates, high demand) and homeowners who were prepared/preparing to sell this spring won’t want to risk the uncertainty of how Coronavirus and the election might change the market 3+ months from now.

The charts below illustrate what new listing volume might look like if half of the homes that were held back from the spring market are released onto the market from July-September and the other half is distributed in-line with the historical monthly distribution through spring 2021.

The Effect of More Inventory

At the end of the day, what everybody wants to know is how changes in market conditions will affect housing prices and buyers’/sellers’ experience in the marketplace.

Right now, prices are appreciating quickly across many sub-markets. An interesting pattern I’ve noticed over the last ~6 weeks is that there seems to be strong market support for modest price appreciation (1-3% over previous market value), but a thin layer of desperate buyers willing to pay significantly more to lock-in a home purchase.

I’ve seen this pattern show up in Arlington in about a dozen multiple offer situations where most offers center around a similar price range (modest appreciation) and one buyer blows everybody out of the water with an escalation that essentially cannot be beaten (with all contingencies waived). I recently had a listing agent inform me that the winning offer included an escalation that “pretty much didn’t end” on a single-family home listed for around $900,000.

This is great for homeowners on the receiving end of this market behavior, but incredibly frustrating for buyers. I think that one benefit of a spike in summer/early fall listings will be the satisfaction of this presumably thin layer of desperate buyers and prices will become more predictable.

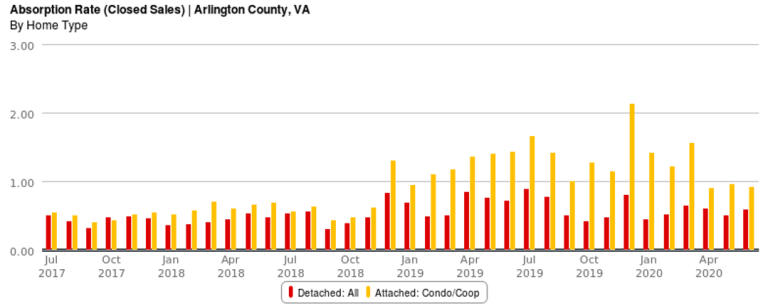

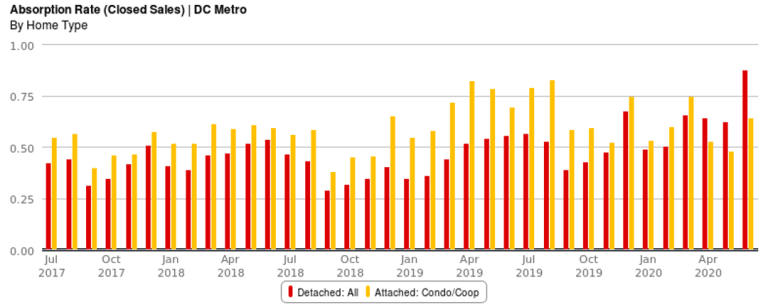

Looking further down the road at the end of 2020 and into 2021, the key metric that will determine how prices react is the absorption rate – the rate of homes sold vs the number of homes being listed for sale. A rate above 1.0 means that demand is outpacing new inventory and there is significant upward pressure on prices. Economists look for an absorption rate of ~0.2 for a balanced market, and the higher the rate, the more favorable the market is for sellers.

Below is the monthly absorption rate for single-family detached homes (red) and condos (yellow) in Arlington and the DC Metro. Note that Arlington’s detached absorption rate is a bit higher if you remove new construction (unfortunately I can’t customize it in this case) and that the Northern VA market is very similar to the DC Metro market.

I expect the absorption rate and demand to remain strong through an increase in new listings which will likely mean continued support for the price growth we’ve experienced so far in 2020.

If you’d like to discuss buying or selling strategies, don’t hesitate to reach out to me at [email protected].