Question: How well prepared is the real estate industry to use technology and innovation to adapt to social distancing?

Answer: With around $2.3T in new and existing home sales in the US in 2019, you would think that the real estate industry would be a catalyst for technology development and innovation to support the purchase and sale of the most valuable asset most people will ever transact.

Unfortunately, that’s not the case and the real estate industry often lags well behind other industries in technology adoption, innovation, and consumer experience. Why is that?

Role of Tech/Innovation in Real Estate

The conversation starts with one critical question – what is the role of technology and innovation in residential real estate? I’ve noticed two schools of thought amongst start-ups and innovators. One is that technology should reduce or eliminate the role of professionals (broker/agent, title attorney, lender) in the transaction and the other is that technology should improve the quality of service and efficiency of those professionals.

I’ll save a lengthy discussion on the value of (professional) real estate agents for another day, but history and many failed start-ups have shown that most consumers want professionals advising them during a home sale or purchase, despite numerous DIY options. I’ll also save commentary on people hiring non-professionals for 6 or 7-figure transactions.

It’s my opinion that the prevailing goal of technology and disruption in residential real estate is to help professionals deliver higher quality service more efficiently, which will in turn improve the experience and reduce cost (commissions/fees) for the consumer. I think it’s important to also improve technology that allows buyers and sellers who prefer a DIY approach, but that isn’t where the lion’s share of investment should be.

#1 Challenge: Fragmented Buying Power

The biggest challenge start-ups face in residential real estate is the fragmentation of the industry’s buying power, which makes widespread adoption difficult and expensive. Most real estate agents are independent contractors who make their own decisions about what systems and technology to pay for so a start-up/entrepreneur with a great idea has to convert tens of thousands (or more) of individuals instead of just a handful of decision-makers with large spending power.

Most agents are loosely organized into offices, brokerages, and brokerage franchises that theoretically have stronger buying power to support start-ups, but it can be difficult to find technology that will be useful for, or adopted by, enough agents and their clients to justify the cost of organization-wide implementation because of so many niche practices and the independent nature of agents.

As they say: technology made for everybody, is good for nobody.

Some brokerages implement top-down in-house technology development and have produced great platforms/systems as a result, but even those technologies lack the disruptive innovation industries need from start-ups because they can’t risk their core business on failed technology development.

Many of the large brokerages that practice top-down technology development suffer from common ailments like expensive systems becoming legacy systems before they generate enough value to justify the cost. The cost of in-house development is too high in many cases, which is why many of the technology/disruptor-branded companies announced the first and largest furloughs/layoffs in the industry just a few weeks into the COVID-19 pandemic.

There is a massive opportunity for disruptive technology in residential real estate, but the fragmented nature of the industry makes it difficult for great start-ups to get off the ground and reach profitability fast enough to survive. This is one reason why VC money has poured into the PropTech (Property Technology, which also includes commercial real estate) industry over the last few years, with investments increasing from $491M in 2013 to $12.9B in the first half of 2019.

Widespread Technology Adoption

Let’s take a look at some of the few real estate innovations that have been implemented on a broad scale to improve the consumer experience and transaction efficiency, that are also supporting social distancing:

- Search: When Zillow brought search to the consumer in 2006, it changed the game by empowering consumers with valuable listing information. As an agent, I appreciate having informed clients because it means I don’t have to deflate dreams of buying a $400,000 six-bedroom mansion in Arlington, Zillow does it for me! I don’t think there’s been a more disruptive and valuable technology in real estate than consumer search.

- Digital Signature: It wasn’t long ago that every offer, counteroffer, and correction required a printer, pen, and scanner/fax but with the widespread implementation of digital signatures contract work has gone from taking hours to minutes and accommodates social distancing.

- 3D Tours: Lightly used prior to the Coronavirus pandemic, 3D tours have become a critical marketing tool during social distancing. It allows interested buyers to explore most nooks and crannies of a home from their phone or computer, limiting the need for physical access (presumably) to only the most interested/motivated buyers.

- Live Virtual Tours: FaceTime, Facebook Live, and other live video applications aren’t unique to real estate but have become popular for virtual Open Houses and showings for buyers who cannot leave their home during quarantine.

Next Generation Technology/Innovation

It’s hard to know what the next true breakthrough in real estate technology will be (or maybe I do!), but I’ll highlight a few things that I’d like to see or expect to see developed in the next decade to improve the consumer experience and transaction efficiency:

- Dynamic/Predictive Search: Home-buying decisions aren’t binary, they’re weighted/sliding scale decisions, yet search is relatively binary and close-ended. Meaning you either want a pool or you don’t. You want 3-4BR and to spend $X-$Y. Current search options don’t consider the weighted value of different criteria and if/then nature of trade-offs people make, so I’d like to see search become more dynamic and help people search the way they think.

- Immersive Virtual/3D Tours: Most people are doing 3D tours from their phone or computer screen, but the technology is mostly there to allow those tours to become more immersive through Virtual Reality headsets. I envision a day when buyers do 15 showings in three hours with their agent from their respective living rooms, using shared immersive virtual technology to tour the properties together. Once they narrow down the best options, they’ll go to see only the top choice(s) in person.

- Augmented Reality: We’ll likely see this coupled with more immersive virtual reality but soon you’ll be able to rapidly redecorate and remodel virtually

- Blockchain: This one warrants more than a few sentences of discussion, so I’ll let this article from the National Association of Realtors do the talking for me.

- Virtual Closings: While many states, including Virginia, allow virtual closings using an e-notary (no in-person signing required) banks have yet to get on-board so, in most cases, the only transactions that can close virtually are cash deals. There’s no doubt that COVID-19 will accelerate banks’ acceptance of virtual closings and eliminate the need for both parties to meet with a title attorney or notary to sign documents in person to consummate the sale.

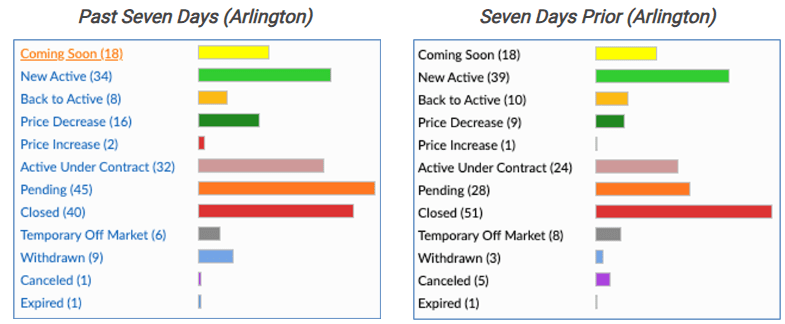

Arlington Market Update

I don’t want to miss my check-in on the Arlington market during this critical time, so here’s a look at the last seven days of market activity compared to the previous seven days.

We took a huge hit in total inventory over the past week with a decrease in new listings, but a sharp increase in contract activity. This reflects what I’ve personally experienced in the market over the last few weeks which seems to be increasing demand with very little new inventory.

As of 7:30 AM April 28, we only have 231 homes for sale. We averaged 245 for sale in April 2019, which was a historical year for low inventory. Of the 260 homes currently under contract, 134 (51.5%) went under contract within one week.

If you’d like to discuss buying or selling strategies in this market, don’t hesitate to reach out to me at [email protected].