Question: Is the single-family home market still as intense as it was earlier this year?

Answer: In January I’ll do a deep dive into the 2021 market performance with a focus on home values, but this week I wanted to dig into some key supply and demand metrics for single-family, townhouse, and duplex homes in 2021 to highlight how the intensity of the market has shifted over the year.

I’m focusing on the single-family, townhouse, and duplex (non-condo/apartment-style) market here because that was the market that exploded locally and nationwide in the wake of COVID-19. It’s important to note, however, when looking at the Arlington market that we didn’t experience nearly the extreme change as many other regional or national markets because things were already competitive thanks in part to Amazon HQ2 and because COVID-based demand tended to favor less expensive markets and markets that offered more space (land and house).

The trends for Arlington can be summarized below, highlighted by charts to follow:

-

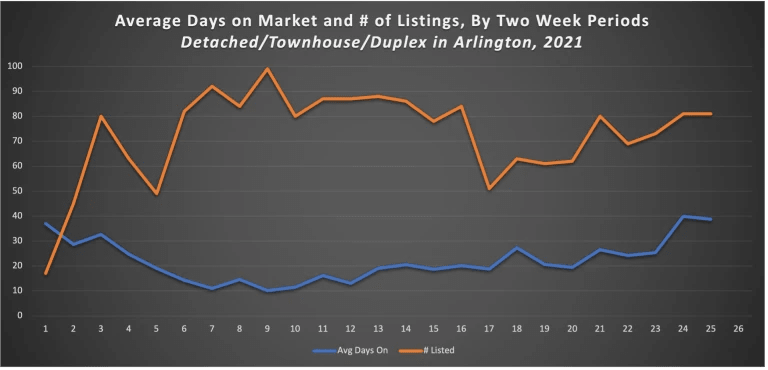

Supply: Supply usually follows a familiar seasonal trend with low supply early in the year, lots of supply coming to market in the spring, followed by a consistent downward trajectory from summer through the end of the year. This year supply did peak in the spring, but maintained a more consistent volume of new supply through the rest of the year, with a surprisingly high number of homes offered for sale in Q4. My best guess for the strong Q4 numbers is that homeowners witnessed such impressive appreciation of their homes in the first half of the year (and second half of 2020) that they wanted to take advantage of current prices instead of timing the market for peak spring demand. It will be interesting to see if this negatively impacts listing volume in 2022.

-

Demand: Demand trends were consistent with their normal seasonal trends, albeit above average through the course of the year. Demand picked up quickly in Q1 and peaked in the spring, followed by a tapering of intensity in the 2nd half of the year. I believe that the tapering of the demand metrics in the 2nd half of the year was a combination of factors including, but not limited to, sellers raising prices based on first-half market performance, many of the most desperate buyers finding homes, buyers dropping out, and buyers focusing less on their home search as vaccines allowed people to return to travel and other plans. I expect strong demand in 2022, but without the crazy price appreciation we had in 2021.

The charts below highlight my supply and demand findings. A few notes on the data that makes up the charts:

-

The data is based on when a property was listed for sale, not when it sold. This gives us an accurate assessment of how the market performed at specific times during the year vs a trailing indicator of demand (using date sold)

-

I broke the year into two-week periods because I think it gives the right perspective on the information we want from the data

-

To aid your reading of the charts Period 5 starts on Feb 21, Period 10 starts on May 2, Period 15 starts on July 11, Period 20 starts on Sept 19, and Period 25 starts on Nov 28

-

I removed new construction from the data because the way it’s listed often doesn’t reflect actual market conditions

-

I removed homes with zero days on the market because they generally reflect a pre-market/off-market deal and they aren’t helpful in this type of analysis

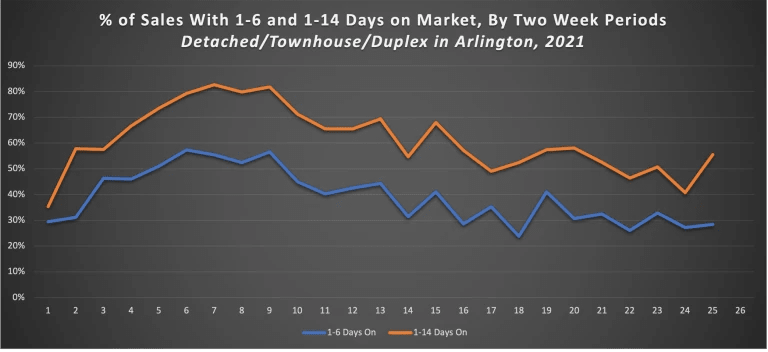

The Market Moved Quickly, Gave Buyers Little Time to Think

Many buyers were forced to make significant purchase decisions in a matter of hours or even sight unseen to secure a good home. During peak spring demand, less than 20% of homes listed for sale sat on the market for more than two weeks and nearly 60% went under contract in less than one week.

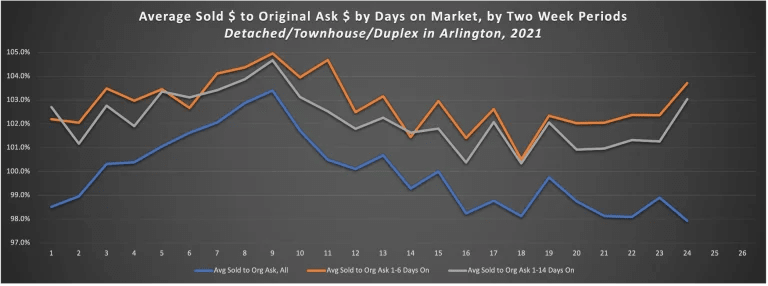

Most Buyers Paid Over Asking Price

On average, buyers paid .2% over the asking price this year and for those who went under contract during a home’s first week on the market, the average buyer paid 2.8% over asking, peaking at an average of 5% over ask in the 9th Period (homes listed April 18-May 1). Remember, these are averages, there were plenty of people paying significantly more than that over the asking price.

Things have gotten slightly more manageable for buyers in the 2nd half of the year with a lot more homes selling at or below asking price, but even with tapering demand, buyers in the 2nd half of the year who go under contract in the first two weeks home was listed paid an average of 1.5% over ask.

Supply Unusually High in 2nd Half, Average Days On Market Increasing

As noted above in my summary, supply volume broke familiar seasonal trends with a consistently strong flow of listings coming to market through the 2nd half and even into Q4. Thus, slightly less demand and unusually high new supply have led to modest increases in average days on the market and less fierce competition.

If you’d like to discuss buying, selling, investing, or renting, don’t hesitate to reach out to me at [email protected].

If you’d like a question answered in my weekly column or to discuss buying, selling, renting, or investing, please send an email to [email protected]. To read any of my older posts, visit the blog section of my website at EliResidential.com. Call me directly at (703) 539-2529.

Video summaries of some articles can be found on YouTube on the Ask Eli, Live With Jean playlist.