Question: Are you seeing different patterns in the housing market slowdown in different parts of the region?

Answer: In September 2020, I wrote an article highlighting how extreme the differences were between the demand shift in Arlington compared to outer suburbs like Fairfax and Loudoun Co. In short, Arlington was competitive before the COVID surge and the outer suburbs lagged far behind it, but once the COVID surge began, Arlington became moderately more competitive while the outer suburbs experienced an extreme shift in market conditions, becoming more competitive than Arlington in just a few months.

Fast-forward two years and we are seeing something of a rubberband effect as the entire housing market slows down, with noticeable shifts in all markets, but more extreme shifts in the outer suburbs. Not that we are witnessing anything close to a crash, the market is still good for sellers, but very different than what we’ve seen the last two years.

Note: this analysis focused on the single-family/detached housing market, not condos or townhouses

Outer Suburbs Slowing Faster, Arlington King of Stability

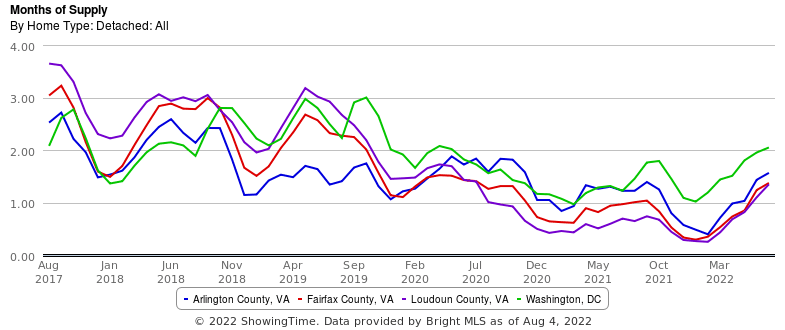

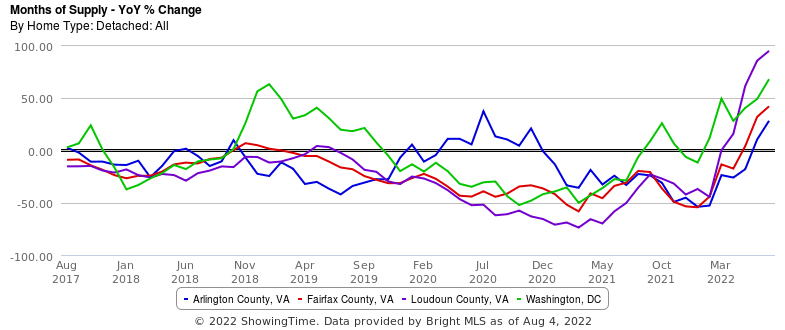

Months of Supply (MoS), a measure of supply and demand that calculates how long existing inventory levels will last based on the current pace of demand (lower levels favor sellers), tells the story better than any other metric.

In the charts below, you can see our regional story of the pre-COVID, COVID, and current real estate market play out:

-

Competition in the outer suburbs generally trailed the DC and Arlington markets, offering buyers more time and leverage in their purchase decisions

-

After Amazon announced HQ2 in November 2018, MoS in Arlington dropped sharply as demand picked up and supply dropped, with a more modest, lagging effect on the surrounding markets

-

The COVID market from roughly summer 2020-spring 2022 sent MoS lower (favorable to sellers) in all markets, but the drop in MoS in outer suburbs was more extreme, pushing those markets well below Arlington and DC, making them extraordinarily competitive

-

As of July 2022, MoS in the outer suburbs was still lower than in Arlington and DC, but rapidly increasing. The year-over-year increase in MoS in Loudoun County was 94.4%, nearly double what it was in July 2021. The increases in MoS were 67.4% (DC), 41.6% (Fairfax Co), and 27.8% (Arlington).

-

You can see the steadiness and strength of the Arlington housing market playout over the past five years in these two charts

Market Shift is Demand-Driven

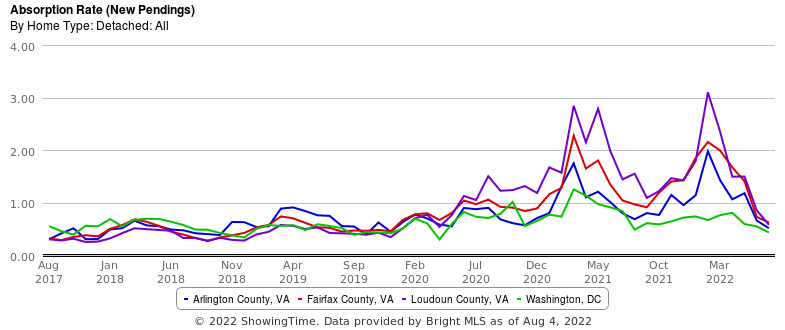

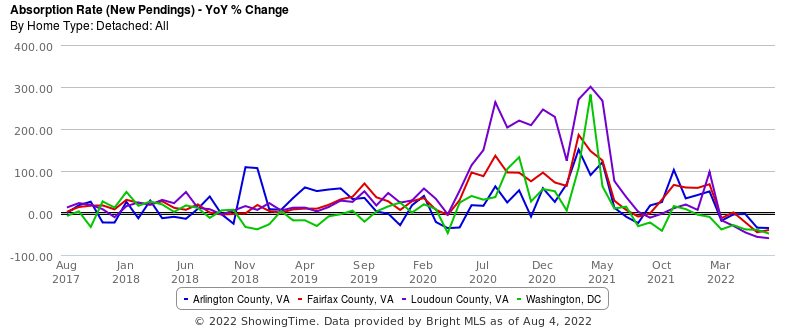

You can blame the sudden market shift almost entirely on a drop in demand, not more listing volume. Absorption Rate (AR) measures the percentage of homes going under contract compared to the number of homes for sale and is a good way of measuring demand.

In the charts below, check out the massive spikes in demand for Loudoun County during the market peaks and the rapid fall over the last few months. You’ll notice in the five-year history that the AR for all four markets shown was pretty similar pre-COVID, and increased far more rapidly in the outer suburbs during the COVID market, but in just the last couple of months, all four markets have come together to their “natural” pre-COVID levels.

The AR in Loudoun Co dropped 60.1% year-over-year in July and Arlington had the lowest year-over-year drop in AR of the four markets, at 35.7%. DC dropped by 48.9% and Fairfax Co. by 40.6%. Loudoun Co capped out at an astonishing 3.1 AR in February, fell to 1.49 by April, and came in at .57 in July. Loudoun and Fairfax Cos remain slightly ahead of Arlington and DC, but I suspect those rankings will reverse in the August/September readings.

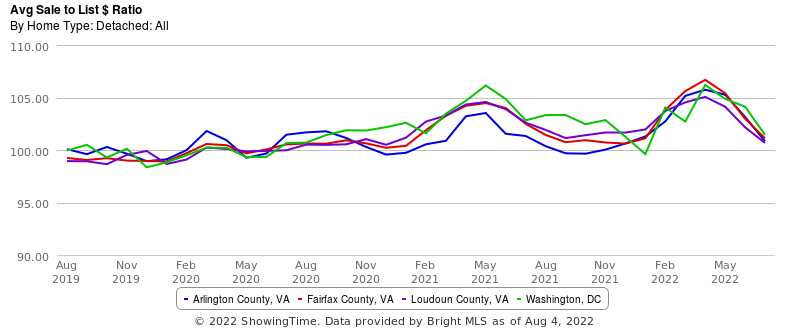

Want another sign of lower demand? The average sold price as a percentage of the asking price has dropped from 105.1%-106.7% in April to 100.7%-101.4% in July. Keep in mind that these are trailing metrics because they are based on sales (usually 3-6 weeks after going under contract), so these are reading from contracts in Feb/Mar and May/June, respectively. I think we will see the average sold price to ask price drop below 100% in most or all four of these markets by the time September data is published, which will reflect contracts from July/Aug.

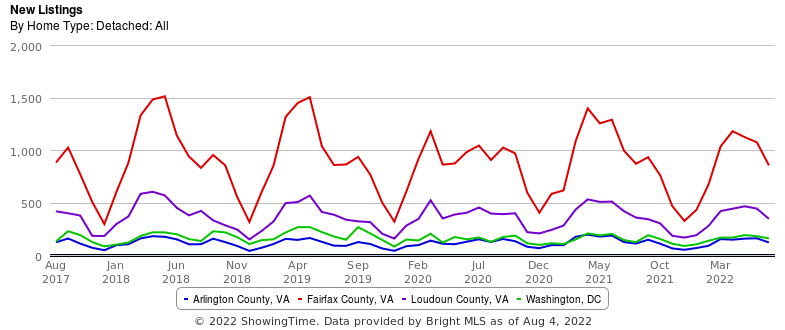

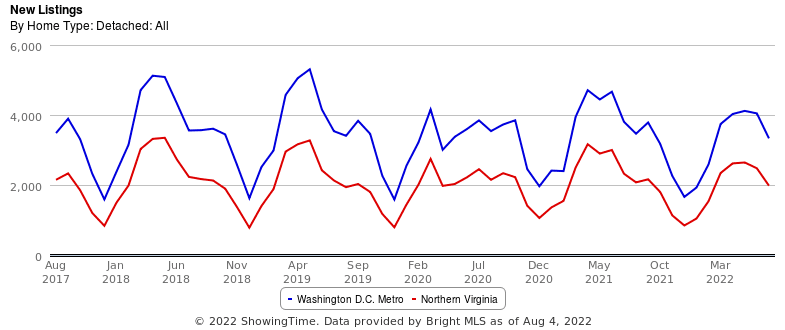

Listing Activity Remains Stable

As noted above, the market shift can be attributed almost completely to lower demand because listing activity remains similar to historical volumes, even down a bit, which is an opposing force on lower demand and helping to maintain a more favorable market for sellers.

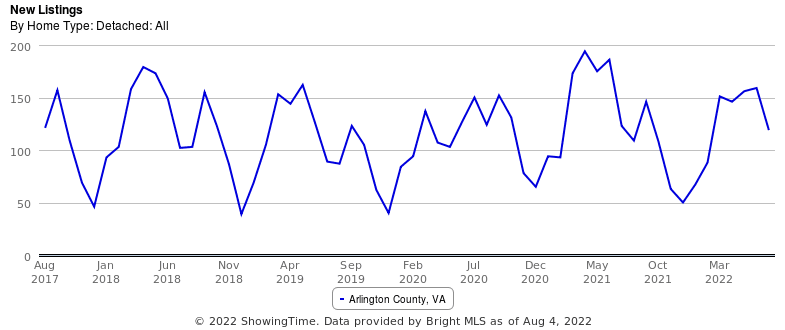

The charts below show new listings of single-family homes in Arlington, Fairfax, and Loudoun Counties, and DC, followed by the same chart for the DC Metro and Northern VA region, and finally a chart just for Arlington since Arlington is a bit hard to see on the first chart. The main takeaway is that across all regional markets, the number of single-family homes being listed for sale has remained steady over the past five years and the fluctuations in market conditions are almost completely driven by changes in demand.

If you’d like to discuss buying, selling, investing, or renting, don’t hesitate to reach out to me at [email protected].

If you’d like a question answered in my weekly column or to discuss buying, selling, renting, or investing, please send an email to [email protected]. To read any of my older posts, visit the blog section of my website at EliResidential.com. Call me directly at (703) 539-2529.

Video summaries of some articles can be found on YouTube on the Ask Eli, Live With Jean playlist.

Eli Tucker is a licensed Realtor in Virginia, Washington DC, and Maryland with RLAH Real Estate, 4040 N Fairfax Dr #10C Arlington VA 22203. (703) 390-9460.