Question: Are the current and future cuts to government jobs and contracts by Trump/Elon Musk/DOGE negatively effecting real estate values and demand?

Answer: With recent announcements of government workforce and contract cuts, led by the Dept of Government Efficiency (DOGE), Elon Musk, and the Trump Administration, many are wondering how these changes impact the local DC-area real estate market. While uncertainty looms, making forecasting difficult, here’s what I’m seeing on the ground and what it could mean for buyers and sellers in 2025 and beyond.

I’m not going to rehash what’s happening in the federal workforce and contractor space because it’s 90% of the news cycle and you can find more detailed and current information across many news outlets, but personally, I’ve followed the excellent coverage of Arlington-based Axios.

Market Remains Strong…

I’ll cut to the chase – so far, in most sub-markets, my team and I have not seen many signals of demand dropping enough to have a measurably negative effect on real estate values. We have been involved in (on the buy and list side), and been privy to, numerous sales with competing offers, escalating prices, and stripped down/out contingencies that have all become the norm during the Q1/Q2 market. These examples have shown up across the Greater DC Area, in different property types (single-family detached, townhouse, and condo), and at various price levels (more on this later).

…Despite Less Market Demand & Intensity

During Q1 of each year, I look closely at the intensity of competition, not just the existence of competition. I define intensity by the percentage of properly marketed and priced homes that are getting multiple offers, the number of offers coming in (this is critical, especially for forecasting the Q2/Q3 market), and how much contract prices are escalating over prior year pricing. The structure of the real estate industry makes this difficult to measure accurately early in the year because it’s more anecdotal than scientific, but I get a feel for it by late-January/early-February and this year market intensity is down from this time last year (and the last five years). It’s hard to say how much of this can be attributed to persistently high interest rates vs the federal workforce cuts.

Note: these are generalized findings, and each real estate sale has its own mini market that can vary from market trends, both positively and negatively.

But it Doesn’t Matter…Yet

There is no doubt that the current and forecasted cuts to the federal workforce and contracts have taken buyers out of the market due to direct job loss/insecurity or indirect fears of future market condition; we have certainly interacted with clients and DC-area residents who have recently suspended or scaled back a home purchase. How many and what percentage of buyers fall into this category is impossible to say at this stage and can vary on a week-to-week basis, and by sub-market.

However, for years, demand has significantly outpaced supply, meaning that most sub-markets can absorb a modest drop in demand without losing value and will remain competitive, especially during times of the year with the biggest mismatch of demand against listing volume.

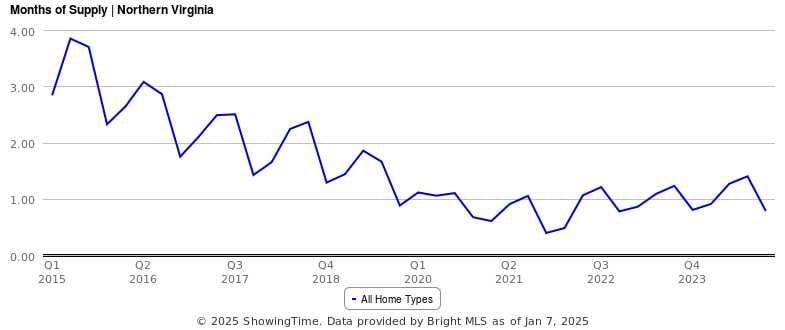

The chart below is a great example of this. It shows Months of Supply (MoS) -- a measure of the pace of demand against current supply levels where lower MoS favors sellers and puts upwards pressure on prices – in Northern VA over the past ten years, by quarter. MoS was 2.32 in Q4 2015 and 0.78 MoS in Q4 2024, a drop of 66% over the past ten years.

What this tells me is that the Northern VA market can absorb a modest drop in demand of 10-20%+ and the effect will most likely be limited to lower appreciation, not negative appreciation (depreciation) as long as the volume of listings coming to market remains similar to’23 and ’24 (likely the case).

Sub-Markets That Can/Cannot Handle Less Demand

I talk a lot about “sub-market” behavior and sub-markets can be defined in many ways – by price range, property type, location, size, age, etc. Different sub-markets experience market shifts/trends in different ways and they will experience the effects of the federal workforce/contracts cuts differently as well.

If you are a buyer or seller involved in or planning to be involved in the 2025 real estate market, I think the most important data points you can look at is supply and Months of Supply (MoS) levels in your sub-market.

Let’s compare some (larger) sub-markets for examples of who has or does not have runway to handle a drop in demand…

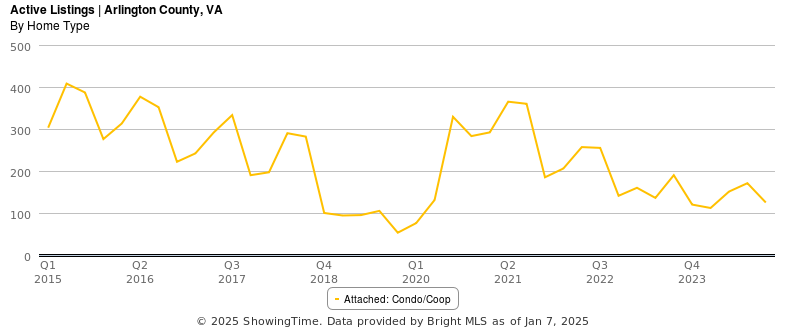

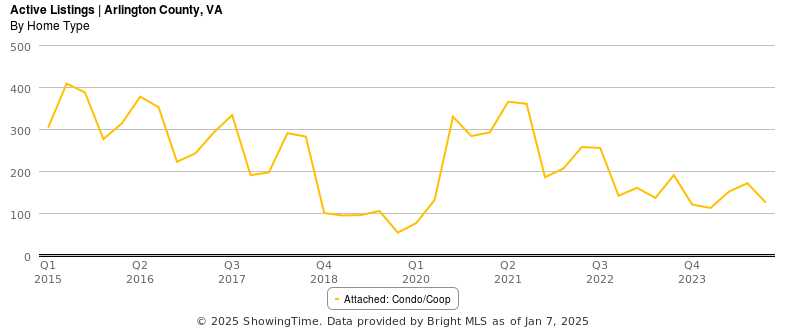

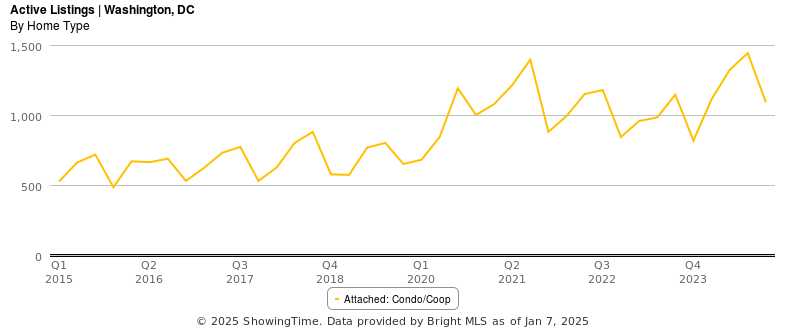

Arlington Condos vs DC Condos: The Arlington condo market should have some runway to handle a drop in demand based on current supply levels relative to the past ten years, but DC condos, a sub-market that was struggling well before cuts to the federal workforce, has supply levels well above the ten year average, and will experience immediate price pain as demand drops.

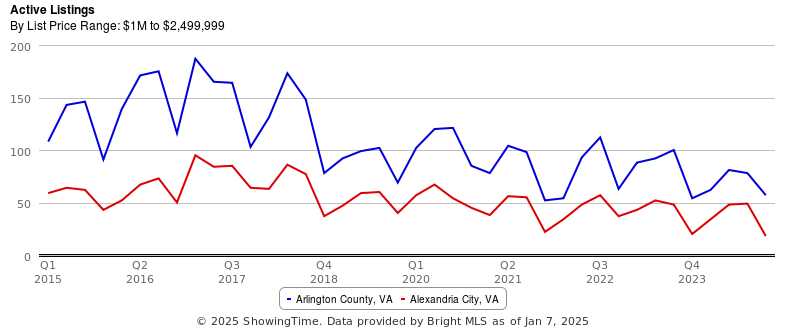

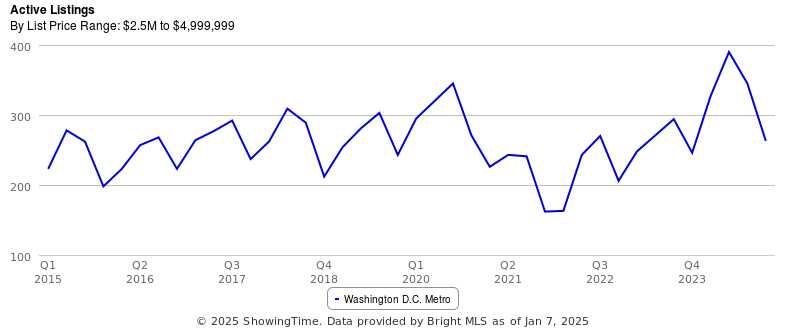

Arlington & Alexandria $1M-$2.499M vs DC Metro $2.5M-$4.99M: The supply of homes in Arlington and Alexandria City in the $1M-$2.5M range is incredibly low and continues to fall, so expect prices to shrug off a drop in demand, for now. This may not be the case for the upper end ($2.5M-$5M) of the DC Metro market comprised of mostly new construction homes concentrated in a handful of affluent neighborhoods, with increasing supply levels over the past three years.

What About Return-to-Office And a Dozen Other Opposing Forces?

We are also kicking off a government-wide Return-to-Office (RTO) requirement that is sending shockwaves through the federal and contractor workforce. I could (and will) write an entire article on RTO, but for today’s article, it represents the tip of the iceberg of major questions/unknowns and opposing forces that will affect the performance of the local real estate market in difference ways such as:

-

Will RTO shift more demand back into the DC Metro housing markets?

-

How long will it take for RTO to show up in the home sale market vs the rental market?

-

Will RTO effect property types (condo vs single-family) in different ways?

-

Will the government workforce/contract cuts hold up or will courts block them?

-

How much, if any, government jobs and contracts will be replaced with new jobs and contracts more aligned to the Trump Admin’s priorities?

-

Will pro-housing policy from the Trump Admin increase demand or supply?

-

Will Trump and Treasury Secretary, Scott Bessent, be successful in their effort to drive down the 10yr Treasury rate (direct correlation to mortgage rates)?

There are a lot of opposing forces at play currently and forecasted in the future which makes the net effect on the local housing market extraordinarily hard to predict, but the importance of good current data and strategic decision-making for buyers and sellers is of utmost importance.

If you’d like to discuss buying, selling, investing, or renting, don’t hesitate to reach out to me at [email protected].

Upcoming (pre-market) ERG Listings, Details and Additional Listings Available by Request

-

Arlington Ridge/Aurora Hills – 3BR/2.5BA/2,450sqft – Detached Single Family (1961) – (ask for street #) S Grove St Arlington VA 22202

-

Williamsburg – 6BR/6.5BA/6,000sqft – Detached Single Family (2025) – 6580 Williamsburg Blvd Arlington VA 22213

-

Courthouse – 1BR+den/1.5BA/850sqft – Condo (2007) – 2220 N Fairfax Dr #308 Arlington VA 22201

-

Cherrydale – 2BR/2BA/1,150sqft – Condo (2013) – 2101 N Monroe St (ask for unit #) Arlington VA 22207

-

Island Creek/Kingstowne – 3BR/3.5BA/2,185sqft – Townhouse (built in 2017) - (ask for street #) Parrish Glebe Rd Alexandria VA 22315

-

Rosslyn/Courthouse – 2BR/2BA/1,000sqft – Condo (2022) – 2000 Clarendon Blvd (ask for unit #) Arlington VA 22201