Question: Is it more effective to save for my kids’ college through a rental property investment or a more typical college savings plan like a 529?

Answer: I often hear from parents who purchase a small investment property around the birth of their child as the primary savings vehicle for college. Some people swear by it. I did it when my son was born (and will report back with results in 13 years!).

I reached out to my financial advisor, Erik Fischer CFP, RICP of Taylor Financial ([email protected], (727) 417-3400), about the topic and he offered a very detailed, thoughtful comparative breakdown of using a real estate investment as a college savings tool vs a more traditional 529. Erik is an excellent resource if you have additional questions about this topic or other financial savings topics.

With frequency, this question arises from parents who gravitate towards real estate investing. And, there is not a definitive answer. Ok – column over. Just kidding. While it’s true that there is not a definitive answer, depending on your situation the answer may be definitive for you.

Identifying the parameters:

-

First, establish a target – how much wealth do you want to save to pay for college?

-

Then, consider the following key areas when comparing the two investment vehicles

-

Savings strategy –how will you fund your savings vehicle

-

Flexibility

-

Level of involvement

-

Associated risks

-

Expected growth rate

-

Tax implications

-

Establish your target:

The good news here is that your target will likely be the same regardless of which approach you choose. So here is an easy-to-follow framework of how to establish your target.

-

Identify the amount you would like to have accumulated for each child when they reach college. You can research the “Cost of Attendance” (*important* this is your all-in cost, not just tuition) at collegeboard.org

-

Use the current cost of attendance for a school and inflate that amount to future dollars using an inflation rate of 5%. Inflate this number out until your child is likely to graduate college.

- Why 5%? This is somewhat arbitrary, but over the last 20 years college costs have been doubling or more than the long-term average inflation rate of 2-3%. I encourage you to use a number somewhere from 5-8%.

- Why 5%? This is somewhat arbitrary, but over the last 20 years college costs have been doubling or more than the long-term average inflation rate of 2-3%. I encourage you to use a number somewhere from 5-8%.

-

Take the last 4 years of inflation-adjusted costs and add them up. These numbers represent a ballpark of what you could expect to pay for this child. Is it perfect? Of course not, but it will give you a greater level of visibility into what you will need.

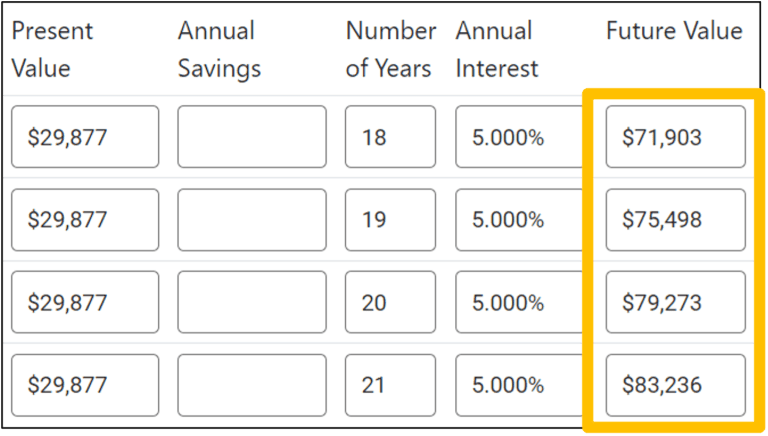

Establish your target (example):

Let’s say your child was just born, plans are to attend college in 18 years and graduate in 4 years. At UVA, the in-state cost of attendance for families making over $110,000 per year is $29,877 (tuition represents roughly half of this number). If you adjust for inflation and add up 4 years of all-in cost, you arrive at an aggregate number that includes the annual timeline of cashflows. See the table below:

These calculations will vary whether you plan for in-state vs out-of-state, public or private, and how much of the cost you are willing to fund. Regardless, the framework will remain the same or very similar to arrive at some accumulation target.

You have your target, now what’s the best way to get there:

Let’s compare a 529-based approach to a rental property-based approach. Of course, these are not the only two ways to save for college, but we’re focusing on these two today.

Let’s first look at the rental property approach:

The high-level idea is buying a rental property when a child is born and selling it to fund college when the child is college-ready.

Because of the increased complexity of rental real estate (which is not inherently good or bad, it just is), let’s identify some of the important considerations first:

-

A down payment will be required

-

Management/execution risk

-

cash flow planning

-

property management

-

tenant management

-

increased tax planning

-

increased insurance planning

-

financing considerations (if you will require a mortgage)

-

a plan to sell the property (to fund college)

-

So, you may have picked up here another hint at what the answer might be for you depending on your situation. That is, if you do not have the cash on hand to make a reasonable down payment for the type of property you desire, the rental property might be off the table for you, at which point you might lean on an annual savings approach of a 529.

Rental property example:

Rental strategies come in all shapes and sizes, but let’s say that we have $50,000 available to fund this strategy and we use that to purchase a property with the following facts:

-

20% down payment, leaving $10,000 left over as a sinking fund to close the deal and maintain the property.

-

Purchase price $200,000

-

Mortgage rate of 6%

-

Cash flow neutral over the 10 years (perhaps negative in the first few years, and positive in the last few years due to rent inflation and fixed mortgage), with annual profits years 11-18 of $5,000 that you let accumulate in a bank account that generates some interest

-

Property appreciates at 3% annually

-

Sell the property in your child’s senior year of high school and pay off the remaining mortgage.

-

Keep the rest in cash to pay for school, or in a high-yield savings or CD ladder to time payments over 4 years. The point is, you’ll have all your cash going into freshman year and you’ll keep it invested safely while they are in college.

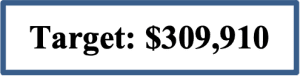

Here is the formula with accompanying visuals below: determine the growth of the underlying asset, then sell after 18 years, subtract 5.5% of the sale price (commissions, closing costs, etc.), eliminate the debt, and add back in the cash from your rental property bank account. Once you have done all this, you are left with unencumbered cash that you can use to pay for college (pay it all to a college…lovely, right?)

$340,487 x 94.5% = $321,760

$321,760 of the take-home transaction, minus the outstanding debt of $94,493 = $227,267

Plus $45,000 in cash that has accumulated in your rental property bank account = $272,267*

*The final available balance will likely be lower due to a capital gains tax, but the tax charge is highly variable based on factors like future tax code, final cost basis, tax management during property ownership, and other personal financial considerations at the time of sale.

We are now very close to our target. Also, it’s very important to identify the many factors that can be quantified with deeper analysis, but by nature are less tangible. Let’s list them:

-

Advantages

- Tax advantages along the way with depreciation, deductible expenses, and favorable tax rates (capital gains rates) on sale

- Opportunity to develop skills and expertise in real estate

- Flexibility that you are not required to use the asset for college if you can pay for or end up choosing to pay for college in some other way – this is a big one.

- Potential for upside return

- Potential to be integrated with planning for your own retirement

- Tax advantages along the way with depreciation, deductible expenses, and favorable tax rates (capital gains rates) on sale

-

Disadvantages

-

The level of management is extremely cumbersome compared to a 529

-

Execution/management risk can significantly impact total returns.

-

Increased Liability

-

Market risk

-

Typically, you will need a significant amount of cash upfront to make the down payment

-

Carefully examine these attributes, because one or some of them might be deal-makers or deal-breakers for you.

Now, let’s compare the rental property strategy to the typical/default college savings account, a 529. This is simple, add an initial lump sum, or deposit annually.

529 – Annual Deposits equaling $500 per month for 18 years

529 – Lump Sum with the same $50,000 that was used for the rental property

The tables above represent the hard numbers that move you much closer to your ideal target. Helpful. Now, many factors can be quantified with deeper analysis, but by nature are less tangible. Let’s identify them:

-

Advantages

- Tax-free growth, and tax-free distributions if used for qualifying educational expenses.

- This is the big one, it’s the main differentiator of the 529 from any other account type.

- This is the big one, it’s the main differentiator of the 529 from any other account type.

- Automatic – set it and forget it

- Can be transferred to other qualifying relatives if needed for their education

- Potential for stock-market returns

- Based on the new Secure Act 2.0 law, part of the plan may be eligible to convert to a Roth IRA for the beneficiary if certain criteria are met

- Tax-free growth, and tax-free distributions if used for qualifying educational expenses.

-

Disadvantages

- Tax benefits are lost if not used for qualifying educational expenses

- 10% penalty on earnings if not used for qualifying educational expenses

- Market risk

- Lack of flexibility to use the money for any other reason, due to a & b above

- Lack of liquidity, use, and control for any reason other than college

- Cannot be integrated with planning for your retirement

- Tax benefits are lost if not used for qualifying educational expenses

Carefully examine these attributes, because one or some of them might be deal-makers or deal-breakers for your situation.

Comparing the two:

How do we put this all together? From a wealth accumulation perspective, in these examples, the rental property strategy wins, and it beats the lump sum deposit into a 529 by a significant amount.

However, this is only one example. If we ran 100 examples for each, we would get 100 different results for each. Yes? You could get a 10% return in the 529, or a 6% return. Your rental property could cash flow negatively in all years, or positively in all years. You could get a great deal or a bad deal. You could refinance if interest rates lower and capture significant savings. You could have an extended vacancy. Maybe the asset only grows by 2% instead of 3%. There will be a ton of variability.

Distill the factors that will influence the results for you:

-

Rental Strategy

- The purchase price of the home

- The plan to sell the home

- Ability to manage the cash flow of a property, maintain it, and sell it properly / advantageously

- Ability to execute proper tax planning along the way

- Ability to manage tenants

- The purchase price of the home

-

529

-

If you deposit a lump sum, at what point in the market cycle did you get started – during a bull market? During a bear market? Unfortunately, this is somewhat out of your control, but it makes a big difference in final results

-

Investment selection – did you create an appropriate portfolio within the account

-

Behavioral finance – did you try to time the market, chase a rate of return, or avoid a market drawdown? As you can tell by the wording, none of those tend to be in your financial interests.

-

What’s the bottom-line(s):

-

Don’t just focus on the surface-level math, but dig deep into the variables that impact your strategy (including non-financial)

-

While real estate in this example, and many others, may produce a higher college savings balance, it comes with a lot more work and requires a large lump sum payment up-front

-

Research and seek out the expertise you need to execute both options efficiently

Thank you very much for your detailed analysis, Erik. I have benefitted from Erik’s financial guidance for many years and would encourage anybody with questions about college savings or other financial planning decisions to reach out to him at [email protected].

If you’d like to discuss buying, selling, investing, or renting, don’t hesitate to reach out to me at [email protected].

If you’d like a question answered in my weekly column or to discuss buying, selling, renting, or investing, please send an email to [email protected]. To read any of my older posts, visit the blog section of my website at EliResidential.com. Call me directly at (703) 539-2529.

Video summaries of some articles can be found on YouTube on the Ask Eli, Live With Jean playlist.

Eli Tucker is a licensed Realtor in Virginia, Washington DC, and Maryland with RLAH Real Estate, 4040 N Fairfax Dr #10C Arlington VA 22203. (703) 390-9460.