Question: Can you provide some clarity on how mortgage forbearance works and whether that will negatively affect my credit score?

Answer: I’ve received quite a few emails from folks considering mortgage forbearance or asking for clarification on (usually) incorrect information provided to them from friends or family about the process. We don’t have all of the answers yet, but enough information is available to help people make more educated decisions about forbearance.

To explain forbearance and some of the unintended consequences, I asked one of the top mortgage lenders in the DC Metro, Jake Ryon of First Home Mortgage, to join as a guest columnist. If you’d like to talk with Jake about a loan, refinance, or any other mortgage related question you can contact him at [email protected].

Take it away Jake…

What is Mortgage Forbearance?

Congress passed the CARES Act, allowing those facing financial hardship due to COVID-19 to request a mortgage forbearance (pause in mortgage payments) for 180 days, with the option to extend for an additional 180 days.

The bill does not require you to provide proof that you’re suffering a hardship, but the CFPB makes it clear that if you can pay your mortgage, you should. However, not everyone is following that guidance and some borrowers who are able to pay are choosing not to and may suffer unintended consequences.

Mortgage forbearance is a temporary pause in payment; it is NOT forgiveness. All missed payments by the borrower must be paid back.

Repayment

Unfortunately, the repayment terms for a forbearance are vague. Statements from Fannie and Freddie indicate that you do not have to repay the missed payments all at once, but that it is for the borrower to work out with the servicer. If the payments are not paid back in a lump sum or over a designated period, but instead added to the end of the loan, the borrower is agreeing to a loan modification.

During a forbearance the servicer (the company you pay) is still advancing the monthly mortgage payments to the end investor. This has led to major issues for lenders, and as a response, tightened credit standards and made it more difficult to obtain a mortgage.

Unintended Consequences

While taking a forbearance is not supposed to negatively affect your credit, there are some unintended consequences I’d like to explain.

*Please note this is based on the most up to date information I could find and is subject to change as this is a fluid situation. Please reach out to your loan servicer directly for your options. *

Refinancing: This may vary by lender, but as I understand it, to be eligible to refinance, borrowers must be out of forbearance and current on their mortgage. This is a big concern if rates continue to fall throughout the year.

Repayment Terms: As mentioned earlier, there are options to repay the missed payments via a lump sum, over a repayment period, or modifying the term of the loan. Keep in mind the servicer must agree to the repayment plan.

I’m hearing that modifications are only being offered if there is documentation to show you’ve been adversely affected by COVID-19. This is going to be problematic for borrowers who didn’t lose their job and assumed their skipped payments would be tacked onto the end of their mortgage or forgiven.

Buying Your Next Home: Since this is so new, we haven’t seen any credit reports reflecting modifications as a result of COVID-19. It’s unclear how lenders and investors will treat these modifications when evaluating new loans.

For example, most investors want to see borrowers pay their mortgage on time for a minimum of 12 months after their modification begins. If someone takes the full 12 months of forbearance, they could be looking at a minimum waiting period of 2 years before obtaining a new loan.

Residual Effects to Your Credit: While the CARES Act says mortgage lenders won’t report you as delinquent during a forbearance, they can’t control how other lenders will view it. For example, if you’re a credit card company and you see a borrower is in forbearance, are you inclined to increase their credit limit or issue a new card? If your credit card debt is increasing and your available line of credit is staying the same or decreasing, it will most likely lower your score.

Weekly Arlington Market Snapshot

Thank you very much for your insights Jake!

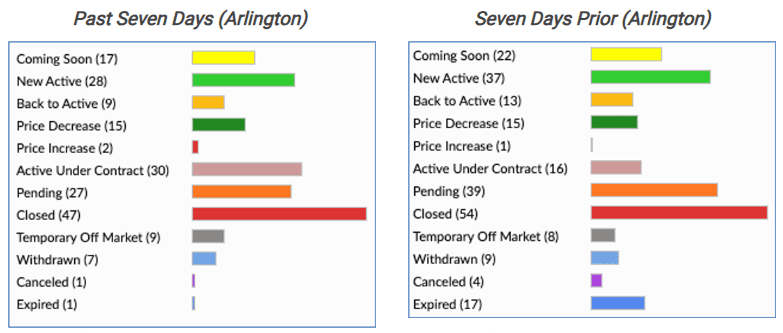

Here’s a quick look at how the Arlington market performed over the past week, compared to the prior week. New inventory and the inventory pipeline dropped down to some of the lowest one-week levels we’ve seen this spring, while contract activity remained relatively strong.

If you’d like to discuss buying or selling strategies in this market, don’t hesitate to reach out to me at [email protected].